The anticipated €16 billion ($17.36 billion) acquisition of Sanofi’s consumer health division by buyout fund Clayton, Dubilier & Rice (CD&R) is stirring excitement among investors and analysts, signaling a potential surge in large private equity transactions across Europe. This deal could mark the beginning of a new era for private equity, driven by a combination of abundant uninvested capital, decreasing interest rates, and the increasing need for asset sales as investors seek better returns.

Recent trends indicate a significant uptick in deal activity. For instance, just this week, a group of investors announced their acquisition of Nord Anglia Education, valuing the British company at $14.5 billion. “We are witnessing a wave of substantial leveraged buyouts in Europe, and there are already several on the horizon,” noted David Gross, co-managing partner at Bain Capital. He emphasized that private equity firms are amassing considerable capital reserves, enabling them to pursue larger transactions.

Henry Frankievich, Managing Director at Insight Partners, highlighted the technology sector as particularly ripe for larger private equity-backed deals. “The driving force behind this resurgence is growth,” he explained. Historically, private equity focused on cost-cutting to optimize margins; however, the current emphasis is shifting toward acquiring businesses with sustainable growth potential.

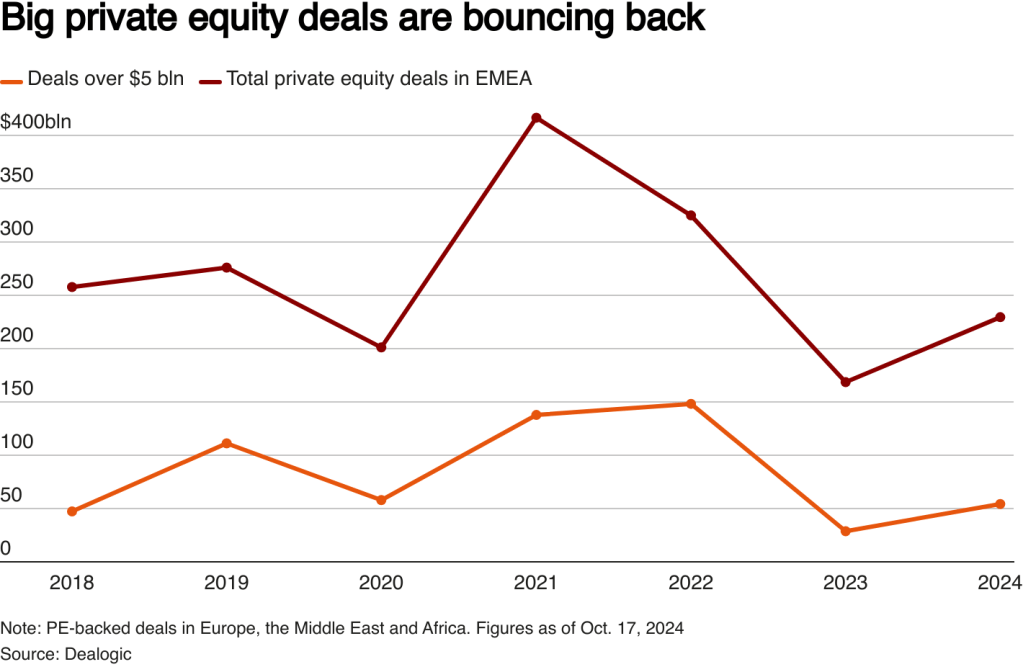

According to Dealogic data, private equity-backed deal volumes in the Europe, Middle East, and Africa (EMEA) region have surged by 41% year-to-date compared to the same period last year. Notably, the number of deals exceeding $5 billion has more than doubled during this timeframe.

On a global scale, buyout transactions are projected to reach $521 billion by the end of this year—an 18% increase from 2023—primarily driven by larger average deal sizes rather than an increase in the number of deals. Despite this recovery, private equity and venture capital funds collectively hold a staggering $2.62 trillion in uncommitted capital as of July 10, indicating a significant amount of “dry powder” waiting to be deployed.

Douglas Hallstrom from Advent International pointed out that while there is an abundance of dry powder in private equity—over 25% being at least four years old—this situation can be concerning. “The age of this capital means it’s becoming increasingly urgent to invest,” he noted. However, he also observed that deal activity is picking up pace. “We’re seeing a revitalization of the transaction environment overall,” he added.

While many traders anticipate further cuts to European bank rates—which would ease financing conditions—some dealmakers remain cautious. Richard Madden, European Executive Chairman at DC Advisory, described a paradox where investors are eager to deploy capital yet hesitate due to perceived risks. “There’s a tension: people are eager to invest but also wary about how risky it might be for their portfolios,” he said.

Madden cited challenges such as difficulties in fundraising and underperformance among certain portfolio companies as reasons for this caution. “When confidence wanes, risk aversion takes hold,” he explained, suggesting that this mindset can hinder investment activity.

Francois Jerphagnon from Ardian echoed these sentiments, stating that only the most robust projects are moving forward in today’s complex environment. “In this challenging landscape, successful initiatives tend to possess both resilience and growth potential,” he remarked.

As we move forward into 2025 and beyond, it seems clear that while opportunities abound in European private equity—especially with the influx of capital and favorable financing conditions—caution will remain a guiding principle for many investors navigating this evolving landscape.